Consolidation Extensions’ Account Configuration Guide

The Account Configuration Guide serves as a preconfigured administrative tool that helps users with specific roles manage accounts effectively. It covers various account groups, including Intercompany, Investment, Capital, Retained Earnings and Non-controlling Interest (NCI), Profit and Loss Treatment, Dividends Paid/Received, and Equity Method – Associates. Users can assign specific elimination rules to the accounts in structured process, mitigating risk of erroneous configuration.

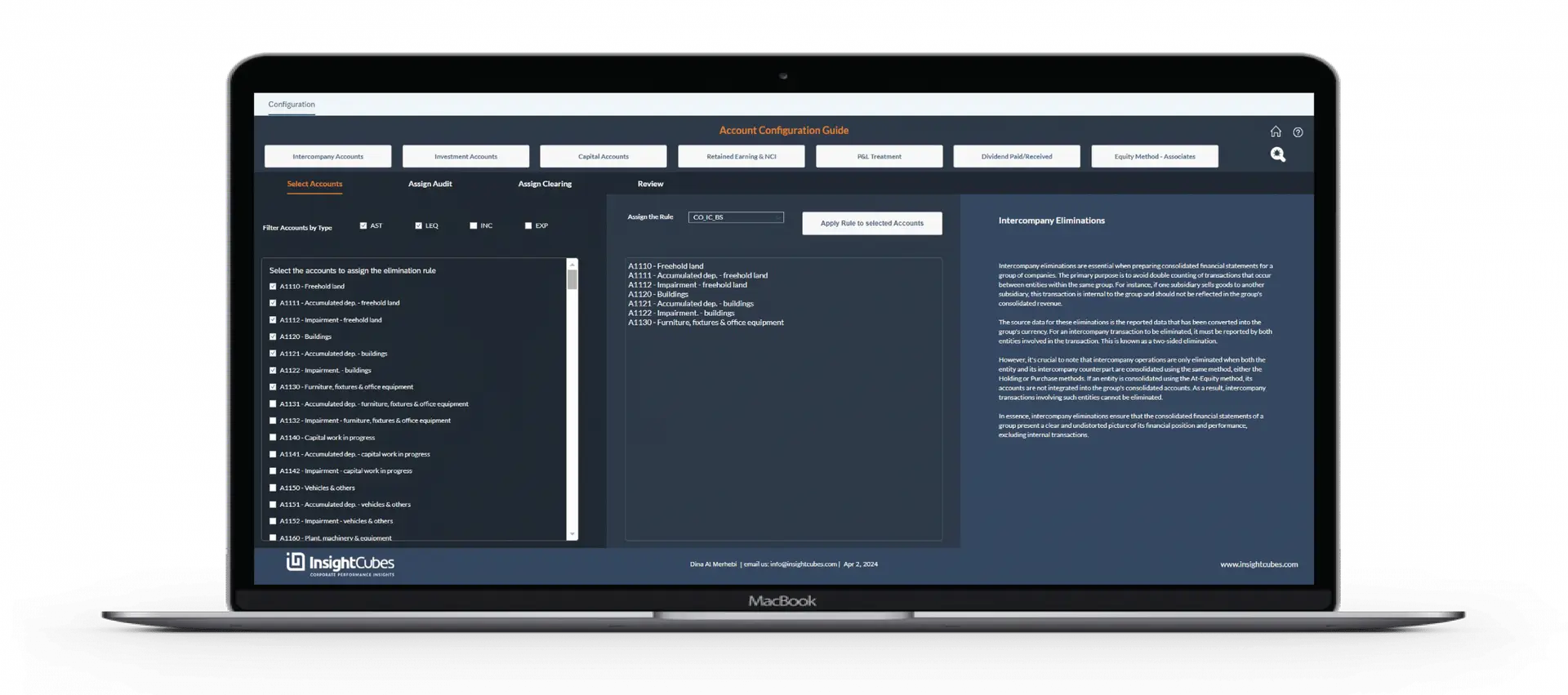

The configuration starts when the user selects the automated elimination type from the button list, then the specific accounts subject to the elimination rule. Additionally, the user can filter the list of available accounts based on account type (Asset, Liability, Equity, Income, Expense). Once you select the desired accounts, you can assign the rule to them from the dropdown menu by clicking the “Apply Rule to Selected Accounts” button.

For each of the selected accounts, the user can assign the receiving Audit Trail member for the automated elimination results based on the rule. If applicable, the user can also assign the clearing account.

Account categories and their associated rules:

Intercompany Accounts

Intercompany eliminations are essential when preparing consolidated financial statements for a group of companies. The primary purpose is to avoid double counting of transactions that occur between entities within the same group. For instance, when one subsidiary sells goods to another, the group does not include the transaction in its consolidated revenue.

The system uses reported data, converted into the group’s currency, as the source for these eliminations. To eliminate intercompany transactions, both entities involved must report it. The system performs a process called a two-sided elimination.

However, it is important to note that the system eliminates intercompany operations only if both the entity and its intercompany counterpart consolidate using the same method, either Holding or Purchase. When a company uses the At-Equity method for consolidation, it excludes the entity’s accounts from the group’s consolidated accounts. As a result, the system cannot eliminate intercompany transactions involving these entities.

In essence, intercompany eliminations ensure that the consolidated financial statements of a group present a clear and undistorted picture of its financial position and performance.

These eliminations exclude internal transactions.

By default, the system assigns the CO_IC_BS rule to the balance sheet intercompany accounts and the CO_IC_PL rule to the Profit and Loss intercompany accounts.

- CO_IC_BS

- CO_IC_PL

- RULE010

- RULE011

- RULE012

Investment Accounts

Because a parent company owns a subsidiary, it records the value of this investment as an asset on its individual balance sheet. In this step, you need to identify the Investment account(s) that contains the investment breakdown between the holding companies and their respective subsidiaries and affiliates, which will be subject to elimination. By default, the CO_INV rule will be assigned to the investment accounts.

- CO_INV

- RULE020

- RULE021

- RULE022

Capital Accounts

The system eliminates capital accounts by offsetting them against the holding company’s investment in the subsidiary. This is a rule, like the Investment Elimination, applicable to holding companies and their subsidiaries; affiliates are not subject to this rule.

In this configuration, the user needs to select the Capital Accounts to be eliminated against the investment value from the Holding Company’s books. If the investment value differs from the Capital Accounts of the subsidiary being eliminated, a clearing account can be used to record the differences. The clearing account can then be further utilized in goodwill or NCI/RE adjustments.

- CO_EQUITY1

- RULE030

- RULE031

- RULE032

By default, CO_EQUITY1 will be applied to the set of Capital Accounts subject to full elimination.

Retained Earning and NCI

Retained earnings and Non-Controlling Interest (NCI) represent two important components of a company’s equity. A company keeps a portion of its net income as retained earnings and does not pay it out as dividends. They represent the cumulative profits or losses of the company since its inception, minus any dividends paid out to shareholders.

Non-Controlling Interest (NCI), on the other hand, refers to the portion of equity in a subsidiary company that is not owned by the parent company. It represents the ownership stake held by external shareholders or minority investors in the subsidiary.

NCI is reported separately on the consolidated financial statements to distinguish it from the equity attributable to the parent company’s shareholders.

- CO_EQUITY2

- RULE040

- RULE041

- RULE042

By default, CO_EQUITY2 is assigned to the Retained Earning account, and the clearing account of the Retained Earnings should point to the NCI account.

Dividends Paid/Received

Dividends paid and received refer to the distribution of earnings by a company to its shareholders. When a company pays dividends, it distributes a portion of its profits to its shareholders as a return on their investment. Alternatively, when a company receives dividends, it earns income from its investments in other companies’ stocks. Dividends paid appear as cash outflows, and dividends received appear as cash inflows in the financial statements. Unlike dividends payables or receivables, the system eliminates dividends paid or received in three steps: it adjusts the P&L, updates Retained Earnings on the equity side (flow F06), and modifies the investment on the asset side.

- CO_DIVIDENDS

- RULE060

- RULE061

- RULE062

By default, the system applies CO_DIVIDENDS to the P&L accounts for dividends paid and received.

Equity Method/Associates

The equity method and associates refer to the accounting treatment used when a company holds significant influence, but not control, over another company. Under the equity method, the investing company recognizes its investment in the associate on its balance sheet and adjusts it periodically to reflect its share of the associate’s profits or losses and dividends received. When a company owns 20% to 50% of another company’s voting shares, it accounts for that company as an associate using the equity method instead of consolidation. This method allows the investing company to accurately reflect its economic interest in the associate’s financial statements.

- EM_CO_EQUITY1

- EM_CO_EQUITY2

- EM_CO_INV

- RULE100

- RULE101

- RULE102

Therefore, when the same investment account records investments in affiliates and subsidiaries, you can omit this step, since the system automatically identifies the ownership method.